Project Details / 项目资讯

- GitHub URL / GitHub 链接: Time-Series-Directional-Change-Analysis

Description / 描述

In the traditional time series analysis paradigm, one would sample prices at fixed intervals, whereas the Directional Change (DC) paradigm is essentially a data-driven approach where the data informs the algorithm when to sample prices.

By looking at price changes from another perspective, it is believed that one can extract new information from data that complements what is oberserved under the traditional time series analysis paradigm. This new information can be utilized by machine learning techniques in order to infer regime information about the market, which in turn helps in the development of algorithmic trading strategies.

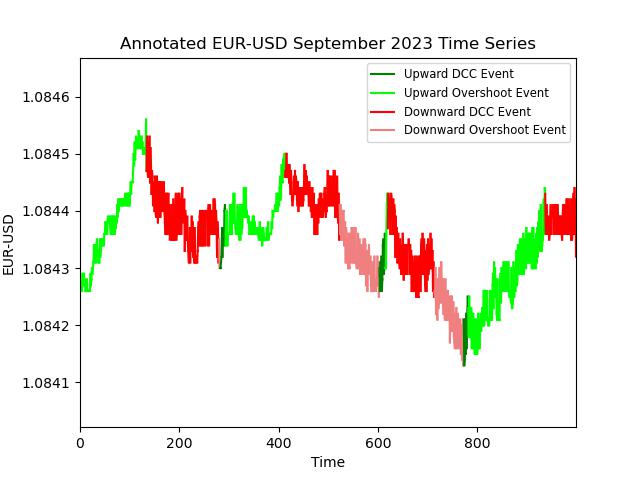

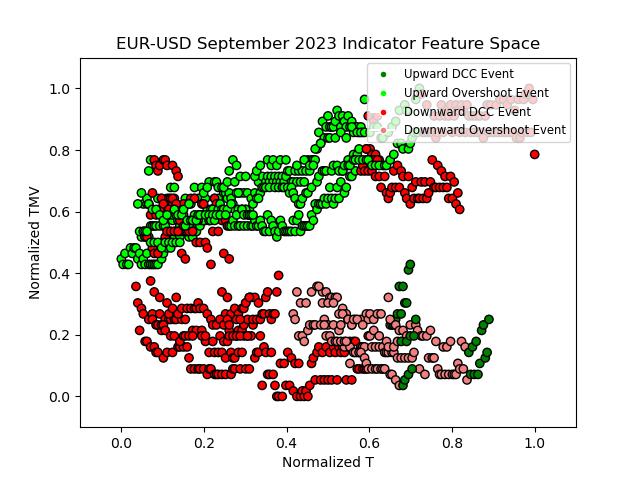

The key DC events of interest are upward Directional Change Confirmation (DCC) event, upward overshoot event, downward DCC event, and downward overshoot event, whereas the variables Total Price Movement (TMV) and Time for Completion of a Trend (T) are the variables of interest which can be fed into a machine learning algorithm to identify regimes/detect regime changes.

在传统的时间序列分析范例中,人们会在固定的间隔处对价格进行采样,而方向变化(DC)范例本质上是一种让数据主导算法何时采样价格的数据驱动的算法。

人们能从另一个角度观察价格变化,以便从数据中提取出与传统时间序列分析范例下所观察到的信息互补的新信息。这些新信息可以被机器学习算法利用,以推断出市场的制度信息,从而助于算法交易策略的开发。

值得关注的 DC 事件包括上升方向变化确认(DCC)事件、上升超调事件、下降 DCC 事件和下降超调事件,而总价变动(TMV)和趋势完成时间(T)是可以输入到机器学习算法中以识别制度/检测制度变化的重要变量。

Reference

[1] Chen, J., & Tsang, E. P. (2020). Detecting regime change in computational finance: data science, machine learning and algorithmic trading. CRC press.